Read this article in Spanish → Leer en Español

Winter Storm “Fern”: Why the $115B headline matters—and what it means for insurance

Date: January 28, 2026

Sources: Insurance Journal (Jan 27, 2026), AccuWeather (Jan 26, 2026), Reuters (Jan 26, 2026), Insurance Information Institute (Jan 26, 2026).

Summary

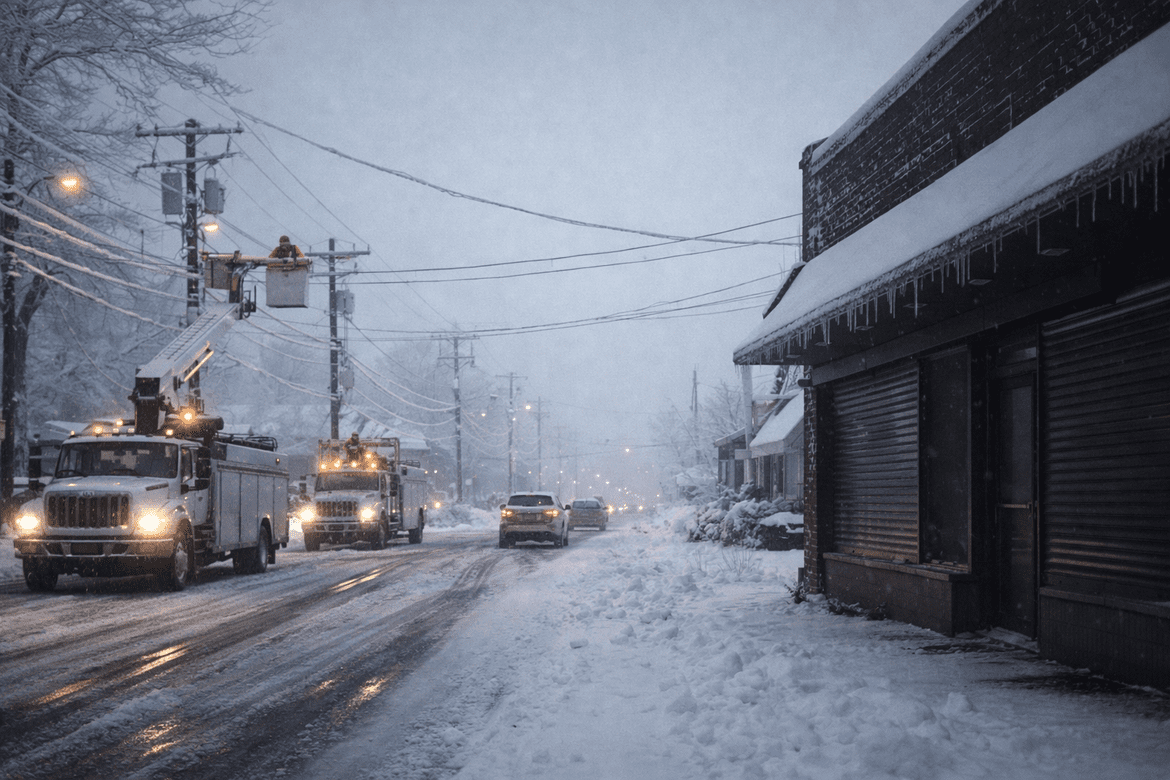

Winter Storm “Fern” disrupted travel, utilities, and commerce across a wide footprint. AccuWeather estimated $105–$115 billion in total economic losses, while industry commentary suggests insured losses are expected in the billions. Understanding the gap between those numbers helps explain what’s typically covered—and what often isn’t.

What happened

AccuWeather released a preliminary estimate of $105–$115B in “damage and economic losses” tied to Winter Storm “Fern.” This kind of figure usually includes both direct property damage and indirect impacts like closures, delays, lost productivity, supply chain disruption, and prolonged power issues.

Travel disruption added to the broader economic hit, with significant flight cancellations and delays reported during the storm’s peak.

Economic losses vs. insured losses

Big headlines often refer to total economic losses, which combine two very different buckets:

- Insured losses: what insurance carriers actually pay, subject to deductibles, limits, exclusions, and cause of loss.

- Uninsured losses: costs that don’t fall under coverage (certain shutdown costs, some outage-related losses, deductibles, or excluded causes).

So while total economic losses may be above $100B, insured losses can be much lower—often reported separately and influenced by policy terms and the specific cause of damage.

The role of insurance

Winter storms typically trigger claims across multiple lines (coverage depends on policy language and cause of loss):

Home / Property

- Ice/snow-related damage and fallen trees.

- Water damage from frozen/burst pipes when policy conditions are met.

- Sudden and accidental damage scenarios (policy-dependent).

Auto

- Collision claims from hazardous road conditions.

- Certain weather-related damage depending on comprehensive coverage.

Commercial

- Building, equipment, and inventory damage.

- Potential business interruption when operations stop due to a covered physical loss (not automatic for every outage or precautionary closure).

Business Interruption: coverage that may help replace lost income and pay certain ongoing expenses when a business must suspend operations due to a covered loss.

Why it matters to you

- The financial hit isn’t just repairs: closures, delays, and logistics disruptions can be costly.

- Extreme cold creates secondary losses: frozen pipes and water damage often show up after the storm.

- Cause of loss drives coverage: similar damage can be treated differently depending on how it happened and what the policy says.

Closing takeaway

Fern is a reminder that winter weather can become a major financial event fast. A general understanding of how home, auto, and commercial coverages respond can make the next storm less disruptive.

CTA (Quantico Insurance): Quantico Insurance can help you review your policies (home/auto/commercial) so you understand—at a general level—what may be covered and what may not before you need to file a claim.

Disclaimer: This article is general educational information, not legal advice or personalized coverage guidance.